WRITTEN BY

Benjamin Zavitz

CFP, CLU

Having a (grand) child is awesome. They expand your thinking as you try to understand their reasoning for items such as; why apple slices are hidden under the couch for future snacks or why one must dress-up like a princess when going to the grocery store. While they may not look like they need it now, today is the perfect time to start putting money away for their education. The two options available are an RESP or a Scholarship Plan.

Registered Education Savings Plan (RESP)

The overall rules of an RESP are:

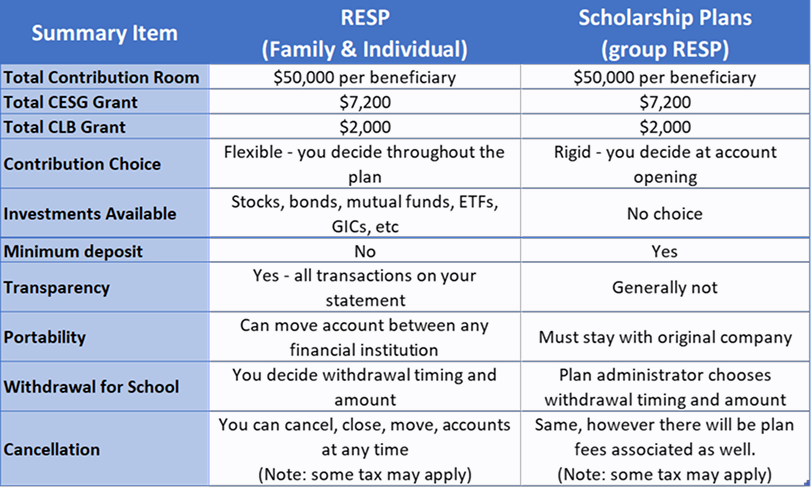

• The maximum lifetime contribution amount is $50,000 per beneficiary.

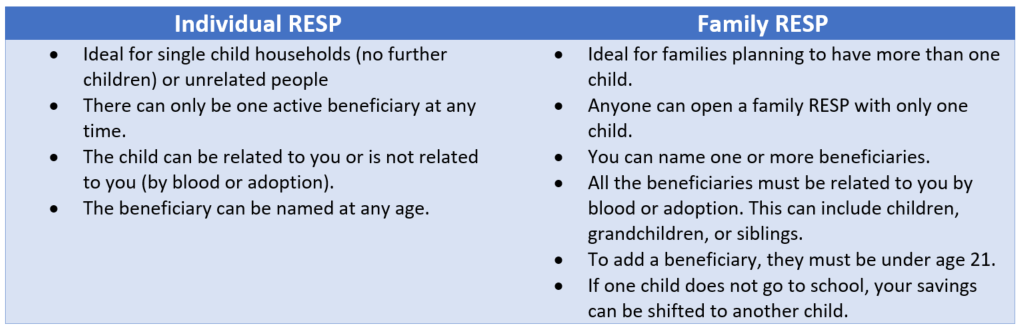

• There are two sub types of RESP’s – individual and family (more details below).

• Education can be an apprenticeship, college, or university (click here for the full list of institutions).

• You (and your financial advisor) choose your RESP investments such as stocks, bonds, mutual funds, ETFs, GICs, etc.

• You may make contributions whenever you choose – very flexible.

• Accounts are portable between financial service companies.

• Contributions do not qualify as a tax deduction.

• By opening an RESP, you have automatically applied for the Canada Education Savings Grant (CESG), and Canada Learning Bond (CLB). More details below.

Canada Education Savings Grant (CESG)

• Available to everyone regardless of family income.

• The government matches your contributions with 20% in FREE MONEY (it’s not a trap, we swear)!

• The maximum annual grant received per beneficiary is $500. That would be a $2,500 contribution from you ($208 per month, per beneficiary).

• Your child will qualify for the CESG until the end of the year they turn 17, so long as by December 31st of year the beneficiary turns 15, there was either a cumulative contribution of $2,000; or $100 contributions over any four years.

• You can carry-forward room that you did not maximize.

• The total lifetime grant is $7,200 per beneficiary (or $36,000 in contributions from you).

Canada Learning Bond (CLB)

• The CLB applies specifically to low-income families. The specifics can be found HERE.

• No personal contributions to an RESP are required to receive the CLB (simply open the account).

• The government will contribute a total of $2,000 per beneficiary. It is $500 for the first year and $100 per year after eligibility is no longer met (child turns 15 or is no longer deemed low-income).