WRITTEN BY

Benjamin Zavitz

CFP, CLU

People hate two things: discussing their own mortality and buying something intangible that provides a benefit they will never experience. I am no different and found a strong dislike when reviewing my own personal life insurance coverage. Even being in the life insurance industry, I could have been quicker implementing this essential coverage.So strap in – welcome to the best self-proclaimed life insurance blog you’ll read today (we hope)!

What is Life Insurance and How Does it Work?

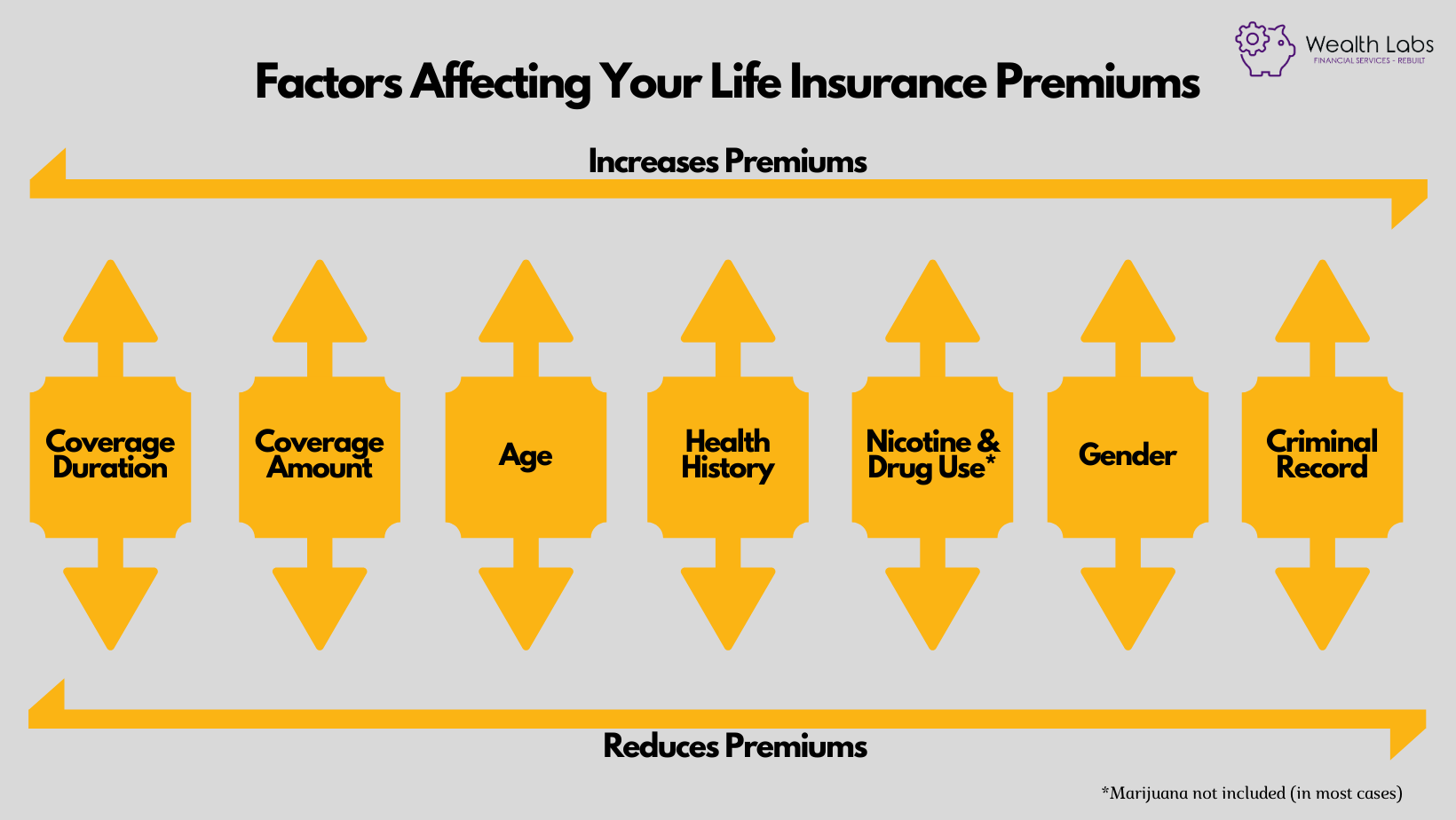

Of all types of insurance, life insurance is the easiest to describe. When you die, the life insurance company pays money to the people you have designated as your beneficiaries. There are no requirements or strings attached to the money, and it is (generally) tax-free to spend as you wish! The life insurance company calculates your mortality risk using data of similar people (age, health, lifestyle, etc.), and that “risk” is how your premiums are calculated.

Common Types of Life Insurance

Of all types of insurance, life insurance is the easiest to describe. When you die, the life insurance company pays money to the people you have designated as your beneficiaries. There are no requirements or strings attached to the money, and it is (generally) tax-free to spend as you wish! The life insurance company calculates your mortality risk using data of similar people (age, health, lifestyle, etc.), and that “risk” is how your premiums are calculated.

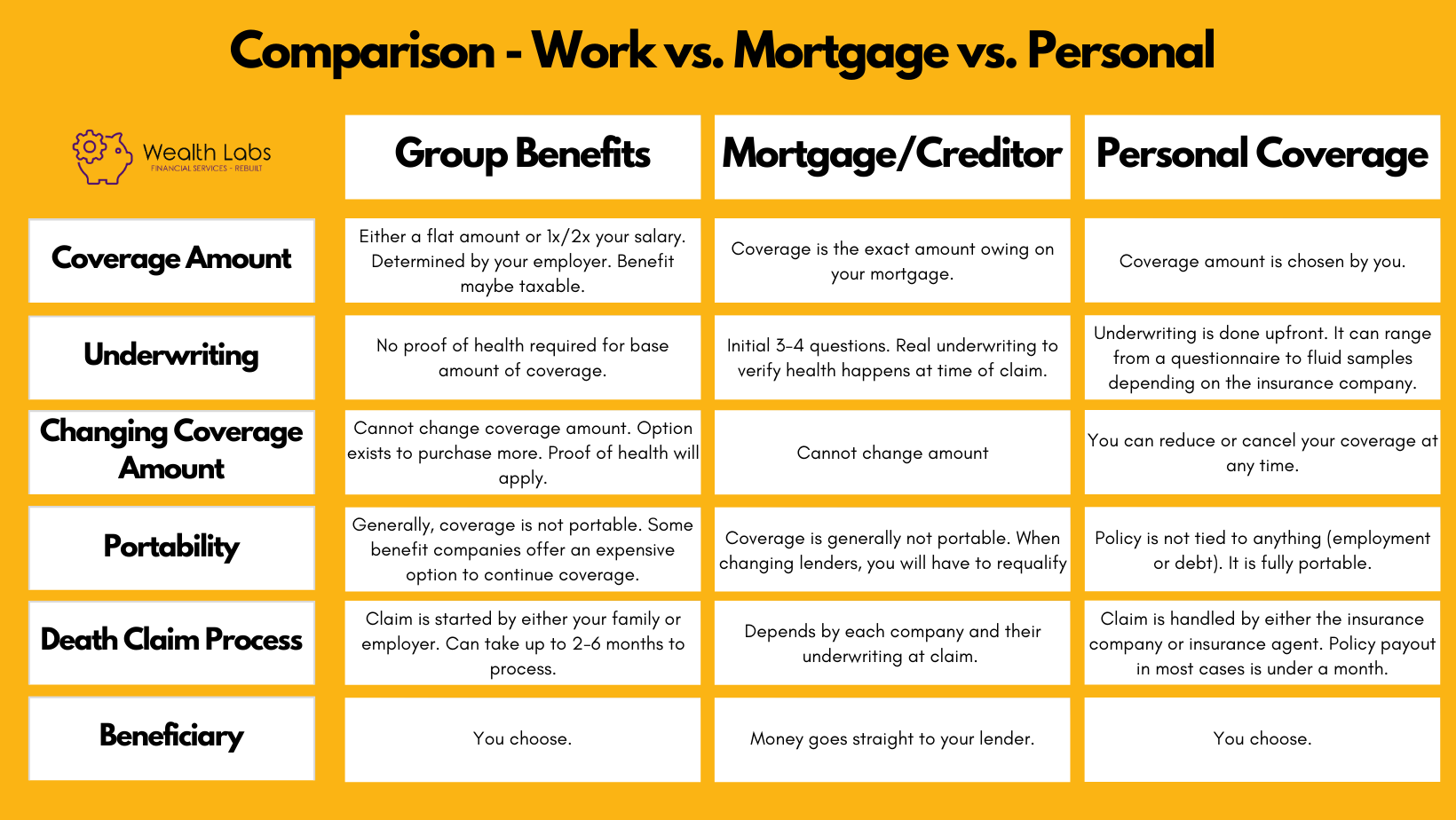

1.) Coverage Through Work

If you have Group Health Benefits through work, there is usually a life insurance component. Frequently, we see a flat rate such as $25,000 - $100,000, or 2x your salary up to a limit. This type of insurance does not require underwriting for each individual. This is because the risk is spread across a larger group of individuals.

Will your benefit payout be reduced by taxes?

This is one of the very few situations where a life insurance payout could be taxable. There are two ways to verify your life insurance benefit will not be taxable when paid to your beneficiaries:

1. Your paycheque shows a deduction for life insurance premiums.

2. You are issued a T4A at tax time. Box 119 is filled in with a dollar amount.

Who controls the coverage?

Your coverage is not owned or controlled by you; it is controlled by your employer. As a result, your employer can increase or decrease your coverage at any time.

Can I take the coverage with me?

This coverage is not portable. If you change employers, the current coverage at your current rate will not be accessible. Depending on the company facilitating your coverage, they may offer a policy that allows you to maintain some form of coverage without underwriting. These plans offer limited coverage and are expensive. This is because almost everyone who chooses to continue their coverage would not qualify for traditional personal coverage, making the entire class of people insured a higher risk.Coverage through your employer has a place in your financial plan. The key is understanding your actual overage and needs. An example is if your current requirement is only to pay for a funeral and final expenses.